/perspectives/sector-views/high-yield-and-bank-loan-outlook-october-2024

Fed Rate Cuts Are Positive for Leveraged Credit (With a Few Caveats)

Effects of rate cuts on high yield bonds may be mixed.

High Yield and Bank Loan Outlook

Fourth Quarter 2024

The effects of the Federal Reserve’s (Fed’s) inaugural interest-rate cut and anticipated future cuts have begun to materialize, but the benefit to the credit markets will vary meaningfully by sector and issuer.

We remain constructive on higher quality, high yield bonds. Carry in this sector is still elevated, and credit fundamentals for many issuers have benefited from securing favorable financing terms during the historically low interest rate environment in 2020 and 2021. The flip side of locking in these low rates is refinancing risk when this debt matures over the next several years at potentially higher market rates.

Leveraged loan borrowers, meanwhile, are poised to benefit more directly from the Fed’s monetary easing due to the loans’ floating-rate nature and continued repricing of contractual spreads lower. Meaningful dispersion in credit quality across borrowers, however, necessitates rigorous credit selection.

We see slightly better relative value in bank loans now, given the higher implied returns available to those with the expertise to differentiate across credits. As the Fed eases rates, bank loan yields will decline while high yield corporate yields are likely to remain largely unchanged, potentially making the value proposition more balanced.

Report highlights:

- While overall financial conditions have eased in response to rate cuts, the benefits to credit may be muted, particularly in the high yield corporate bond market, which is likely to absorb higher interest rates for several years as existing low interest-rate debt gets refinanced.

- In the near term, the refinancing burden for high yield issuers is manageable, with just 4 percent of the total market maturing in 2025, and 9 percent due in 2026.

- High yield corporate bonds and leveraged loans currently offer attractive yields of 7 percent and 9 percent, respectively. We slightly favor loans, given better implied returns available to those with the expertise to differentiate across credits.

Macroeconomic Outlook

Markets Respond Positively to Rate Cuts, Although Benefits to Credit May Be Modest

The Fed kicked off its easing cycle with a 50-basis point rate cut at its Sept. 18 Federal Open Market Committee meeting, noting it had gained greater confidence in achieving its 2 percent inflation target and was attentive to emerging labor market risks. Fed Chair Jerome Powell characterized the move as a recalibration of policy from restrictive levels in order to maintain labor market strength. Markets responded positively to the move, with equities rallying and credit spreads tightening modestly. While market-implied rates shifted lower in 2024, they rose in 2025, suggesting a marginal decline in recession expectations.

While overall financial conditions have eased in response to Fed rate cuts, the benefits to credit may be muted by “locked-in” effects across some fixed-rate credit channels, including in the mortgage market, the investment-grade corporate bond market, and the high yield corporate bond market.

In particular, the high yield market may continue to absorb higher interest rates for several years as existing debt matures. In contrast, lower coupon payments may offer some relief from elevated rates in the loan market, although these reductions are unlikely to significantly improve credit profiles for highly leveraged borrowers. Corporate earnings will likely play a bigger role in determining interest coverage ratios going forward. Therefore, a key aspect of the credit outlook will be the Fed’s success in achieving a soft landing, which remains our base case view but is a far from certain outcome.

While we continue to view a soft landing for U.S. growth as the most likely outcome with the Fed lowering interest rates to a neutral level of 3.25–3.5 percent by the end of 2025, our outlook carries downside risk due to the softening labor market. Although the September jobs report came in stronger than expected, we see weaker signals from consumer perceptions of job availability and business surveys. Declines in immigration flows and less support from fiscal policy will further weigh on growth, as we discussed in our recent Quarterly Macro Themes. In this environment, a prudent approach for investors is to safeguard portfolios with careful credit selection, while capitalizing on the yield opportunities that credit markets offer.

Effect of Rate Cuts on High Yield Bonds May Be Mixed

We remain constructive on higher quality, high yield bonds given the still-elevated carry in this sector and positive credit fundamentals for many issuers. Yet, borrowers are unlikely to benefit further from falling interest rates as their debt—issued in a historically low rate environment—matures and must be refinanced at higher market yields.

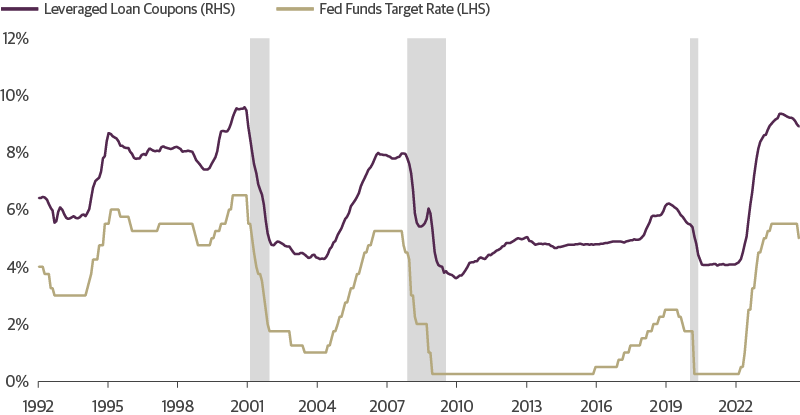

High yield corporate bond yields have declined more than 100 basis points from their year-to-date high in April, sliding from a peak of 8.3 percent to just 7 percent as of the end of the third quarter of 2024. But many issuers capitalized on the low interest rate environment in 2020 and 2021 to secure favorable financing terms, so their average coupons of 6.3 percent remain notably below market yields. This gap provided a buffer against the effect of aggressive rate hikes and elevated borrowing costs from 2022 to 2024.

High Yield Corporate Bond Yields Remain Above Average Coupons

Source: Guggenheim Investments, Bloomberg U.S. Corporate High Yield Bond Index. Data as of 9.30.2024. Gray areas represent recession.

A portion of this debt will need to be refinanced in coming years, given the five- to seven-year maturity profile of most high yield corporate bonds, and companies face the prospect of refinancing at higher rates. Consequently, for the Fed’s easing cycle to directly benefit the fundamentals of existing borrowers, high yield corporate bond yields would need to decline further from their current levels.

Treasury yields have largely priced in expected rate cuts, limiting the potential for further declines. A more aggressive easing cycle could drive yields lower, but this scenario would likely occur in worse than anticipated economic conditions and would be accompanied by wider spreads. High yield credit spreads, currently near historically tight levels at around 300 basis points, have limited room to tighten as they are below the 10th percentile of historical valuations.

In the near term, the refinancing burden for high yield issuers is manageable. Only $45 billion in maturities are due in 2025, or just 4 percent of the total market, and $110 billion is set to mature in 2026, representing another 9 percent, and the majority of these maturities are rated B- or above. This market structure limits potential maturity-driven default risks.

Given our view that there is limited room for yields to decline further, we expect the majority of returns in the high yield corporate bond market to come from coupons. Returns driven by spread compression would be another potential source of performance, but this is constrained for BB- and B-rated bonds, which are in their 7th percentile of historical valuations. In contrast, even though CCC-rated spreads tightened from 940 basis points at the start of third quarter to 642 basis points by quarter end—reaching their tightest levels since March 2022—they are still in their 30th percentile of historical valuations.

Two reasons the CCC-rated cohort has lagged the broader high yield spread rally is due to its higher leverage profile (by definition) and its larger exposure to the communications sector. Based on the public universe, the median CCC leverage was 12x and the interest coverage ratio was only 1.2x at the start of 2022 before the Fed began raising rates. This put the group at a large disadvantage as we entered the hiking cycle, contributing to our theme of market bifurcation along the lines are larger, higher quality companies and smaller, highly leveraged companies. These ratios have improved somewhat to 9.6x leverage and 1.6x interest coverage, but not without many defaults and distressed exchanges over the past two years clearing out the weakest links.

As a capital intensive and often higher leveraged industry, operators in the communications space faced a multitude of challenges over the last five years: consumer cord-cutting trends, weak cash flows, fierce competition, a tighter fundraising environment, and high borrowing costs. A major bifurcation emerged between large and small communications companies, as larger companies had more levers to pull to navigate the environment. Given consumer trends, another divide emerged between companies that had wisely focused on wireless connectivity in recent years. Communications has grown to become 36 percent of the CCC-rated index from 15 percent at the end of 2020. For the BB-rated sector and B-rated sectors, communications comprises just 12 and 13 percent, respectively.

Higher Quality Leveraged Loan Issuers Stand to Benefit Most from Rate Cuts

Leveraged loan borrowers are poised to benefit more directly from the Fed’s easing cycle due to their loans’ floating interest rates, as well as continued repricing of contractual spreads lower. Credit quality across borrowers is significantly dispersed, however, and overall quality is relatively low, making credit selection crucial. Over time, leveraged loan returns will likely decline along with falling short-term rates, but for high quality credits there is still value in current all-in yields.

Leveraged loans are typically tied to short-term rates like the one-month or three-month Secured Overnight Financing Rate (SOFR). Anticipated reductions in interest rates will swiftly translate to lower borrowing costs for issuers. When SOFR declines, loan coupons will reset lower, providing immediate cost savings.

Loan Issuers Should Benefit from Rate Cuts as Borrowing Costs Decline

Source: Guggenheim Investments, Bloomberg, Federal Reserve, Credit Suisse. Data as of 9.30.2024. Gray areas represent recession.

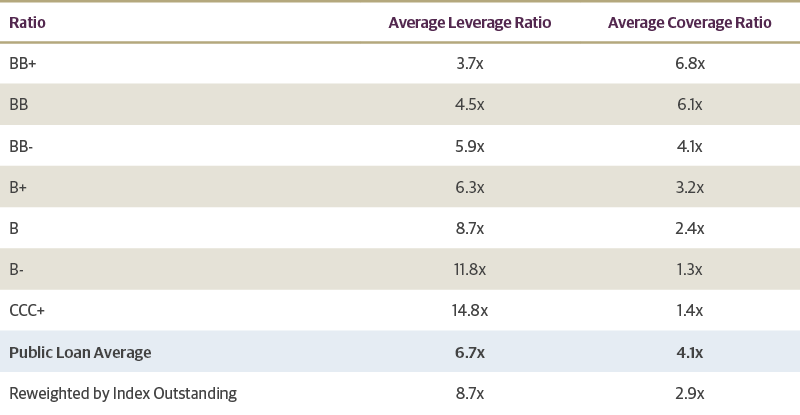

The public leveraged loan market has a healthy average interest coverage ratio of around 4.1x, suggesting that many issuers can comfortably meet their interest payments. Only 15 percent of the loan market is public, however, and the ratio represents a subset of issuers that are mostly BB-rated, creating differences with the broader Credit Suisse Leveraged Loan Index. When reweighting average coverage ratios based on outstanding par value or the number of loans outstanding, we estimate that the true average coverage ratio for the loan market is closer to 2.9x, more than a full turn lower than suggested by public data.

Public Loan Issuer Credit Ratios

Source: Guggenheim Investments, Capital IQ, Credit Suisse. Data as of 6.30.2024.

Furthermore, there is significant dispersion within the market. Higher rated issuers (BB+) boast much stronger coverage ratios, averaging around 6.8x, while lower rated issuers (B- or CCC+) have coverage ratios of just 1.3x and 1.4x, respectively. This variation underscores the different levels of risk across the credit spectrum.

This year the loan market has seen robust repricing activity, with issuers of loans trading above par seizing the opportunity to reduce their borrowing costs. Year to date, weighted average contractual spreads have narrowed by 25 basis points, resulting in cumulative annual savings of approximately $3.5 billion for loan issuers (0.25 percent on a $1.4 trillion market). The full benefit of this may not yet be fully reflected in interest coverage ratios, as these metrics are reported on a trailing 12-month basis.

Further cost savings may be possible. Roughly 30 percent of the loan market trades above par, potentially allowing some issuers to opportunistically tap the market again to reduce their borrowing costs. While contractual spreads are aligned with their 10-year average, there remains room for tightening. Much of this will depend on collateralized loan obligation (CLO) demand for leveraged loans.

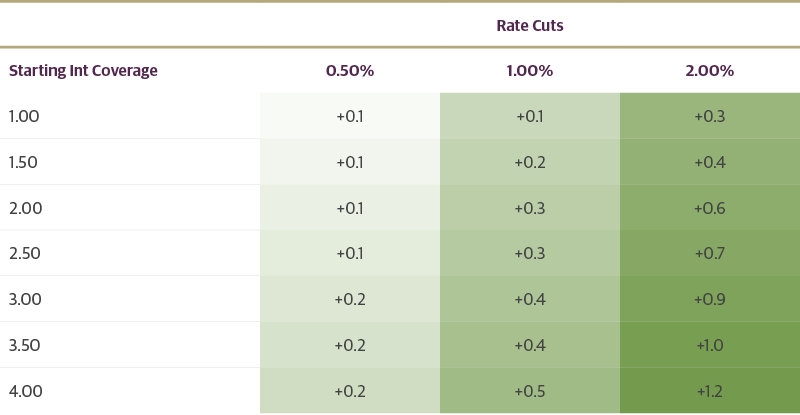

The cumulative effect of potentially falling coupon spreads and the Fed’s expected rate cuts should provide relief to loan issuers over the next 18 months. A 200-basis-point reduction in SOFR could further improve interest coverage ratios across the market, particularly for higher rated issuers with stronger balance sheets. For borrowers with low starting coverage ratios (closer to 1x), such a reduction would only marginally improve their position to 1.4x, holding earnings equal, leaving them still vulnerable to default or necessitating liability management exercises.

Rate Cuts Benefit Those Starting Off in a Healthy Position

Changes in interest under various rate-cutting scenarios.

Source: Guggenheim Investments, Credit Suisse. Data as of 9.15.2024. Analysis isolates the effect of rate cuts by assuming only coupons change but all else is equal, including earnings.

The bottom line: While the Fed’s easing cycle is likely to benefit loan issuers, the rewards will not be evenly distributed. Higher rated issuers stand to gain the most, while lower rated issuers with weak interest coverage ratios may continue to struggle even with lower borrowing costs.

Investment Implications

High yield corporate bonds and leveraged loans currently offer attractive yields of 7 percent and 9 percent, respectively. We slightly favor loans now, given the better implied returns available for those with the resources and expertise to differentiate across credits. As the Fed eases rates, though, bank loan yields will decline while high yield corporate yields are likely to remain largely unchanged, possibly bringing the value proposition into balance.

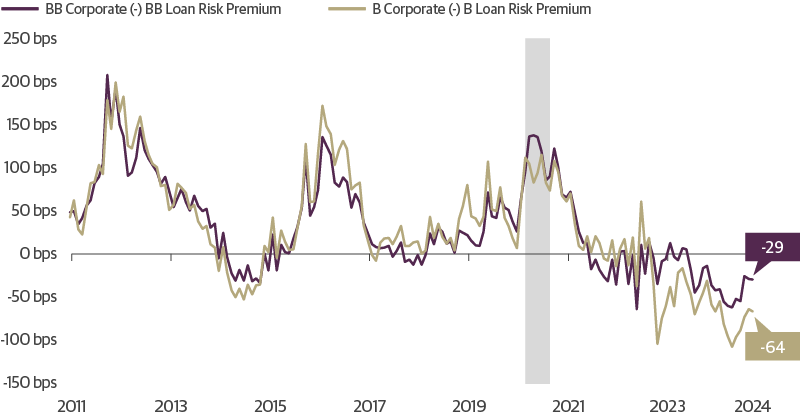

High yield corporate bond spreads are tighter relative to their historical averages than bank loan discount margins across every rating. For example, single B corporate bonds are in their 7th percentile of historical levels, while single B bank loans are in the 43rd percentile. And on an absolute basis, bank loans discount margins are wider than bond spreads for every comparable rating.

Bonds may be relatively more expensive than loans in part due to differing credit loss expectations. The market-implied default rate is 5.4 percent for loans and 1.2 percent for bonds, using average recovery rates of 50 percent for loans and 40 percent for bonds. Over the past 12 months, however, the loan default rate has been lower than implied by these spreads. The Credit Suisse Leveraged Loan Index has a default rate of 2.6 percent, and 2 percent for the BofA High Yield Index. These figures suggest the market expects additional stress in loans but a decline in bond defaults. Based on this analysis, we view the average relative value proposition slightly tilted toward bank loans but see active credit selection as essential.

High Yield Corporates Trade Richer than Bank Loans

Source: Guggenheim Investments, Bloomberg, Credit Suisse. Data as of 9.30.2024. The difference in risk premium is measured based on corporate bond nominal spreads to Treasuries and bank loan four-year discount margins. Gray area represents recession. Past performance does not guarantee future results.

Diversification across high yield and leveraged loan sectors can enhance portfolio resilience against unexpected shifts in the outlook. For instance, if the easing cycle falls short of market expectations, corporate bond performance could suffer amid upward yield shifts, while a well-curated loan portfolio could offer relative insulation in higher quality credits.

While both high yield bonds and leveraged loans offer value, investors should prioritize quality, focusing on higher rated issuers and maintaining senior positions in the capital structure. In the current environment, rigorous credit selection is crucial for navigating potential risks and capitalizing on opportunities.

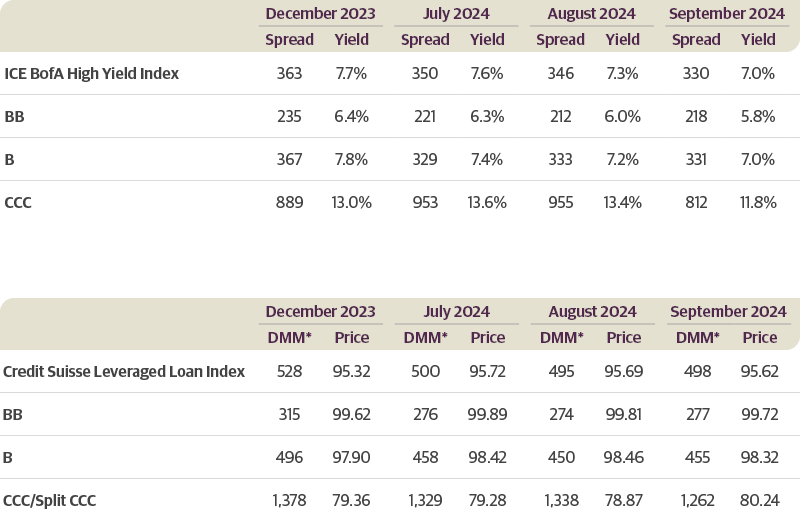

Leveraged Credit Scorecard

As of 9.30.2024

Source: ICE BofA, Credit Suisse. *Discount Margin to Maturity assumes three-year average life. Past performance does not guarantee future results.

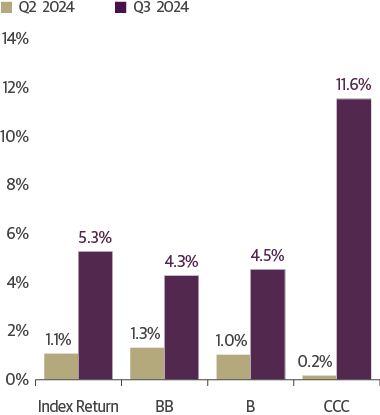

ICE BofA High Yield Index Returns

Source: ICE BofA. Data as of 9.30.2024. Past performance does not guarantee future results.

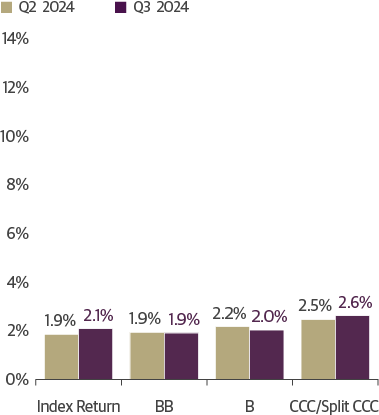

Credit Suisse Leveraged Loan Index Returns

Source: Credit Suisse. Data as of 9.30.2024. Past performance does not guarantee future results.

Important Notices and Disclosures

INDEX AND OTHER DEFINITIONS

The referenced indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

The Credit Suisse Leveraged Loan Index tracks the investable market of the U.S. dollar denominated leveraged loan market. It consists of issues rated “5B” or lower, meaning that the highest rated issues included in this index are Moody’s/S&P ratings of Baa1/BB+ or Ba1/ BBB+. All loans are funded term loans with a tenor of at least one year and are made by issuers domiciled in developed countries.

The ICE BofA U.S. High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. In addition, qualifying securities must have risk exposure to countries that are members of the FX-G10, Western Europe or territories of the US and Western Europe. The FX-G10 includes all Euro members, the U.S., Japan, the UK, Canada, Australia, New Zealand, Switzerland, Norway and Sweden.

A basis point (bps) is a unit of measure used to describe the percentage change in the value or rate of an instrument. One basis point is equivalent to 0.01 percent.

AAA is the highest possible rating for a bond. Bonds rated BBB or higher are considered investment grade. BB, B, and CCC-rated bonds are considered below investment grade and carry a higher risk of default, but offer higher return potential. A split bond rating occurs when rating agencies differ in their assessment of a bond.

The three-year discount margin to maturity (DMM), also referred to as discount margin, is the yield-to-refunding of a loan facility less the current three-month Libor rate, assuming a three year average life for the loan.

The interest coverage ratio is a debt and profitability ratio used to determine how easily a company can pay interest on its outstanding debt.

The leverage ratio is a metric that expresses how much of a company’s operations or assets are financed with borrowed money.

Spread is the difference in yield to a Treasury bond of comparable maturity.

Investing involves risk, including the possible loss of principal. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. Longer term bonds are more sensitive to interest rate changes and subject to greater volatility than those with shorter maturities. During periods of declining rates, the interest rates on floating rate securities generally reset downward and their value is unlikely to rise to the same extent as comparable fixed rate securities. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

This article is distributed for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This article is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

©2024, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim Partners, LLC. For information, call 800.345.7999 or 800.820.0888.

Member FINRA/SIPC GPIM 62751 GI-FIO 1024

Tune in to Macro Markets to hear the top minds of Guggenheim Investments offer timely analysis on financial market trends. Guests include portfolio managers, fixed income sector heads, members of the Macroeconomic and Investment Research Group, and more.

Guggenheim Investments represents the investment management businesses of Guggenheim Partners, LLC ("Guggenheim"). Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim.

Read a prospectus and summary prospectus (if available) carefully before investing. It contains the investment objective, risks charges, expenses and the other information, which should be considered carefully before investing. To obtain a prospectus and summary prospectus (if available) click here or call 800.820.0888.

Investing involves risk, including the possible loss of principal.

*Assets under management is as of 12.31.2024 and includes leverage of $14.8bn. Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Wealth Solutions, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Private Investments, LLC.

This is not an offer to sell nor a solicitation of an offer to buy the securities herein. GCIF 2019 and GCIF 2016 T are closed for new investments.

©

Guggenheim Investments. All rights reserved.

Research our firm with FINRA Broker Check.

• Not FDIC Insured • No Bank Guarantee • May Lose Value

This website is directed to and intended for use by citizens or residents of the United States of America only. The material provided on this website is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation. Investing involves risk, including the possible loss of principal.

By choosing an option below, the next time you return to the site, your home page will automatically

be set to this site. You can change your preference at any time.

We have saved your site preference as

Institutional Investors. To change this, update your

preferences.

United States Important Legal Information

By confirming below that you are an Institutional Investor, you will gain access to information on this website (the “Website”) that is intended exclusively for Institutional Investors and, as such, the information should not be relied upon by individual investors. This Website and any product, content, information, tools or services provided or available through the Website (collectively, the “Services”) are provided to Institutional Investors for informational purposes only and do not constitute a recommendation to buy or sell any security or fund interest. Nothing on the Website shall be considered a solicitation for the offering of any investment product or service to any person in any jurisdiction where such solicitation or offering may not lawfully be made. By accessing this Website, you expressly acknowledge and agree that the Website and the Services provided on or through the Website are provided on an as is/as available basis, and except as partnered by law, neither Guggenheim Investments and it parents, subsidiaries and affiliates nor any third party has any responsibility to maintain the website or the Services offered on or through the Website or to supply corrections or updates for the same. You understand that the information provided on this Website is not intended to provide, and should not be relied upon for, tax, legal, accounting or investment advice. You also agree that the terms provided herein with respect to the access and use of the Website are supplemental to and shall not void or modify the Terms of Use in effect for the Website. The information on this Website is solely intended for use by Institutional Investors as defined below: banks, savings and loan associations, insurance companies, and registered investment companies; registered investment advisers; individual investors and other entities with total assets of at least $50 million; governmental entities; employee benefit (retirement) plans, or multiple employee benefit plans offered to employees of the same employer, that in the aggregate have at least 100 participants, but does not include any participant of such plans; member firms or registered person of such a member; or person(s) acting solely on behalf of any such Institutional Investor.

By clicking the "I confirm" information link the user agrees that: “I have read the terms detailed and confirm that I am an Institutional Investor and that I wish to proceed.”