/perspectives/portfolio-strategy/policy-volatility-market-opportunity

Don’t Let Policy Volatility Overshadow Market Opportunity

Long-term signals are positive for fixed income.

March 25, 2025

| By Anne Walsh, JD, CFA, Chief Investment Officer, Guggenheim Partners Investment Management

The year has begun favorably enough, with bonds enjoying positive returns and equity valuations still high despite recent declines, but as we move deeper into 2025 it’s clear we’re sailing into uncharted waters. The return of President Trump to the White House has injected a jolt of volatility into not just the markets but the global geopolitical/economic landscape. His unpredictable approach to foreign and trade policy, coupled with an aggressive domestic agenda on immigration, taxes, deregulation, and cost-cutting, has created an environment of policy uncertainty. And let’s not forget that the Federal Reserve (Fed) is keeping the market in suspense about its next monetary policy move pending more clarity on the inflation front. Frankly, in my decades in this business, I’ve rarely seen such a confluence of political and policy uncertainty dominate the investment landscape.

We should brace ourselves for continued volatility as these policies evolve and get implemented. The issue is that with so many policy changes taking place all at once it is hard to predict whether the end result will be stagnation or inflation. The shift in inflation expectations driven by potential tariffs is a key area to watch. In isolation, tariffs are inflationary—or at least that is the conventional wisdom. Tariffs can significantly reshape supply chains, manufacturing, and consumption patterns, and these concerns are already being captured in consumer sentiment. The big questions revolve around the scope of these tariffs, their geographic and industry focus, and their final outcome. Which of the threatened tariffs will be carried out and which are simply negotiating salvoes?

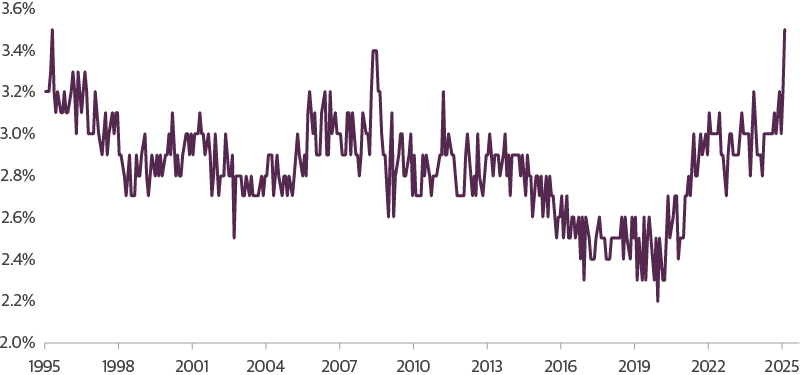

Inflation Expectations Reach Multi-Decade High

University of Michigan Consumer Sentiment Survey: Median Expected Change in Prices During Next 5-10 Years

Source: Guggenheim Investments, Bloomberg, University of Michigan. Data as of 2.28.2025.

The same questions about execution can be asked about deregulation, cost-cutting, and immigration. The Department of Government Efficiency (DOGE) has grand ambitions for cost-cutting—and I have no doubt that there is significant waste and fraud waiting to be uncovered—but we can already see fights with Congress and court battles looming over many of DOGE’s more aggressive moves. Similarly, it is a challenge to quantify the impact of the administration’s immigration policy goals—which include significant border restrictions and mass deportation—on our national workforce, adding another reason for overall market unease.

This game of badminton between politics and policy, reflecting the tension around the administration’s ambitions and the realities of Congressional negotiation, will likely send rates and equity markets rising and falling with every news cycle. In the middle of all this market noise, however, it’s crucial to remain focused on the long-term signals that truly matter. And those signals are pointing in a positive direction.

First and foremost, inflation, while still stubbornly hovering above the Fed’s 2 percent target, has been declining for almost two years, and while recent progress has slowed the overall trend appears to be intact. Some worry about the potential inflationary impact of immigration restrictions on sectors like construction and agriculture, but lower immigration reduces both aggregate supply and aggregate demand, creating ambiguous effects on wages. And tariff announcements can get delayed or changed before they are enforced, or rescinded after they are put in place.

Second, solid economic performance has strengthened credit quality for most issuers. While credit spreads are tight, adjusting them for relative strength in key metrics like leverage and interest coverage shows they are justifiable and could even tighten further. In addition, comparatively higher yields in the U.S. should sustain strong demand across sectors. Investment Grade corporates are yielding north of 5 percent, Investment Grade ABS can be found with yields over 6 percent, high yield bond yields currently exceed 7 percent, and yields on U.S. leveraged loans surpass 9 percent. We anticipate the 10-year Treasury yield to trade within a range of 3.5% to 4.75%, and any movement above 4.5%, particularly towards 5%, would signal a buying opportunity. Both model estimates and the Fed’s own commentary suggests monetary policy is still moderately restrictive, with continued pockets of vulnerability in the economy. That alone should lead to one to two rate cuts by the end of 2025, provided inflation expectations stay under control.

Third, the U.S. economy, despite the political headwinds, remains resilient. This strength, coupled with attractive interest rates, underpins a strong U.S. dollar, making the U.S. market an attractive investment destination.

The U.S. economy entered 2025 with good momentum, and we have a relatively positive outlook, but it is only prudent to consider how our outlook could go wrong. Several scenarios could disrupt the current trajectory. First, there is a risk that a modest inflation uptick could loosen the anchor on inflation expectations, creating a cycle of rising prices and interest rates that would negatively impact growth and asset values. Second, an escalating trade war, particularly with China, could lead to trade partner retaliation, disrupt supply chains, and hurt U.S. exporters, leading to wider credit spreads and equity market declines. Third, the current optimism surrounding AI's productivity enhancements could unwind if reality falls short of expectations. The equity market is highly concentrated in mega-cap tech names reliant on AI to sustain high valuations, and the DeepSeek episode, while short-lived, echoed the tech bubble burst that brought down markets and the broader economy. Finally, a scenario where the Trump administration successfully implements its agenda could lead to sustained growth and lower inflation in the long run but create pain in the short run from deep spending cuts which reduce fiscal spending and economic stimulus and tight immigration policy shrinking the labor force. If anything, our concern is that downside risks from these policy actions, resulting in lower GDP growth, have increased. While we don't anticipate these outcomes in our base case, we remain vigilant and prepared to adjust our strategy as needed.

While President Trump’s policy agenda will undoubtedly make a lot of noise that drives volatility, investors would be wise to focus on the signal provided by a solid U.S. economy, favorable disinflationary trends, and strong credit fundamentals. With moderating inflation, anticipated Fed rate cuts, and attractive yields, now is an opportune time for active fixed-income managers to potentially capitalize on these conditions. We like Investment Grade Corporate and Structured Credit—particularly asset-backed securities (ABS) backed by data centers and their supporting infrastructure—and real assets that will continue to offer income and potential for value appreciation. With so much policy uncertainty, however, we are maintaining a prudent allocation to defensive, higher-quality positions that can provide liquidity should market volatility escalate further.

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to interest rate risk. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. Longer term bonds are more sensitive to interest rate changes and subject to greater volatility than those with shorter maturities. During periods of declining rates, because the interest rates on floating rate securities generally reset downward, their market value is unlikely to rise to the same extent as the value of comparable fixed rate securities. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy or, nor liability for, decisions based on such information.

©2025 Guggenheim Partners, LLC. Guggenheim Investments represents the investment management business of Guggenheim Partners, LLC. Securities offered through Guggenheim Funds Distributors, LLC.

GPIM 64198

Tune in to Macro Markets to hear the top minds of Guggenheim Investments offer timely analysis on financial market trends. Guests include portfolio managers, fixed income sector heads, members of the Macroeconomic and Investment Research Group, and more.

Guggenheim Investments represents the investment management businesses of Guggenheim Partners, LLC ("Guggenheim"). Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim.

Read a prospectus and summary prospectus (if available) carefully before investing. It contains the investment objective, risks charges, expenses and the other information, which should be considered carefully before investing. To obtain a prospectus and summary prospectus (if available) click here or call 800.820.0888.

Investing involves risk, including the possible loss of principal.

*Assets under management is as of 12.31.2024 and includes leverage of $14.8bn. Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Wealth Solutions, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Private Investments, LLC.

This is not an offer to sell nor a solicitation of an offer to buy the securities herein. GCIF 2019 and GCIF 2016 T are closed for new investments.

©

Guggenheim Investments. All rights reserved.

Research our firm with FINRA Broker Check.

• Not FDIC Insured • No Bank Guarantee • May Lose Value

This website is directed to and intended for use by citizens or residents of the United States of America only. The material provided on this website is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation. Investing involves risk, including the possible loss of principal.

By choosing an option below, the next time you return to the site, your home page will automatically

be set to this site. You can change your preference at any time.

We have saved your site preference as

Institutional Investors. To change this, update your

preferences.

United States Important Legal Information

By confirming below that you are an Institutional Investor, you will gain access to information on this website (the “Website”) that is intended exclusively for Institutional Investors and, as such, the information should not be relied upon by individual investors. This Website and any product, content, information, tools or services provided or available through the Website (collectively, the “Services”) are provided to Institutional Investors for informational purposes only and do not constitute a recommendation to buy or sell any security or fund interest. Nothing on the Website shall be considered a solicitation for the offering of any investment product or service to any person in any jurisdiction where such solicitation or offering may not lawfully be made. By accessing this Website, you expressly acknowledge and agree that the Website and the Services provided on or through the Website are provided on an as is/as available basis, and except as partnered by law, neither Guggenheim Investments and it parents, subsidiaries and affiliates nor any third party has any responsibility to maintain the website or the Services offered on or through the Website or to supply corrections or updates for the same. You understand that the information provided on this Website is not intended to provide, and should not be relied upon for, tax, legal, accounting or investment advice. You also agree that the terms provided herein with respect to the access and use of the Website are supplemental to and shall not void or modify the Terms of Use in effect for the Website. The information on this Website is solely intended for use by Institutional Investors as defined below: banks, savings and loan associations, insurance companies, and registered investment companies; registered investment advisers; individual investors and other entities with total assets of at least $50 million; governmental entities; employee benefit (retirement) plans, or multiple employee benefit plans offered to employees of the same employer, that in the aggregate have at least 100 participants, but does not include any participant of such plans; member firms or registered person of such a member; or person(s) acting solely on behalf of any such Institutional Investor.

By clicking the "I confirm" information link the user agrees that: “I have read the terms detailed and confirm that I am an Institutional Investor and that I wish to proceed.”