Summary

Though the National Association of Insurance Commissioners (NAIC) has fine-tuned its risk-based capital (RBC) formula many times since it initiated the standard in the early 1990s, it is now considering a major overhaul of the required capital calculation. The possibility exists that the proposed changes could require a major reassessment of common stock allocations in investment portfolios and overall business strategies.

The American Academy of Actuaries (AAA) presented a paper to the NAIC in June outlining a structure to complete such a review. While we know from experience that this will likely be a long and bumpy road, at Guggenheim Investments we partner with our clients to prepare for and manage these and other regulatory changes.

In this report, we examine the importance behind the risk correlation assumptions and discuss the possible impact to the investment portfolios of Life and Annuity insurers.

Report Highlights

- Correlation Assumption Review: The NAIC plans to revamp correlation assumptions embedded in its RBC model. In June, an AAA presentation to the NAIC’s Life RBC Working Group outlined a structure to review the correlation assumptions in the RBC formula. In October, the AAA provided a comparison to other capital frameworks globally.

- Micro to Macro Shift: While the NAIC continually reviews individual factors across the entire RBC model, the correlation assumptions that underlie the formula have not been updated since 2001, when investment risks were first bifurcated into fixed-income and equity risks.

- Potential Impact on RBC Ratio: This change could have a major impact on the RBC ratio and the relative value of equity investments made by life insurers. If not calibrated correctly, it could result in 25–50 percentage point changes in RBC ratios across the industry.

- Assumptions Being Reassessed: In the current model, the underlying risk components are either assumed to be 100 percent correlated or independent. This binary assumption will likely change when the NAIC reviews the interactions across all risk components.

- Beginning Stages of the Review with Timing to Be Decided: With the scope and timing of the review still uncertain, the potential exists for wide ranging impacts across the insurance industry. We believe the effects will vary based upon an insurer’s business lines and the composition of its balance sheet. The NAIC intends the update to benefit more diversified businesses, and adversely impact concentrated ones.

Overhauling the RBC Ratio

Functioning as an indicator of insurer solvency, the RBC model has worked as the NAIC intended—to help identify undercapitalized companies. The NAIC continually reviews the model for efficacy and accuracy and fine-tunes it as needed. Updates proceed at varying speeds, although the trend has been toward more rapid tinkering in recent years.

In March 2024, an AAA presentation to the NAIC’s Life RBC Working Group raised the possibility of changing the correlation assumptions underlying the RBC formula. Instead of a targeted change to a factor that impacts a specific asset class, this time around the formula itself is under discussion for update. This would likely have a far greater impact on insurers’ RBC ratios than prior, more pinpointed updates.

Risk Components Included in the RBC Ratio

The RBC model incorporates a variety of risk factors to develop the minimum amount of capital surplus needed given the different risks assumed by an insurer. The RBC ratio compares the extent to which an insurer’s total adjusted capital (TAC) covers its required capital derived from the risk calculations, expressed as a percent.

The model considers risks related to an insurer’s business, underwriting, and investments, and is separated into five broad risk categories, some of which have subcomponents. Each risk included in the model has an associated capital factor, a numerical value that indicates how much capital must be held to support that risk. The NAIC reviews and adds risks it deems necessary.

Five RBC Risk Categories

As asset managers, our primary focus is on risks included in the C-1 investment category: C-1cs (common stock risk) and C-1o (other investment risk—fixed income risk).

Binary Correlation Assumptions Are Under Review

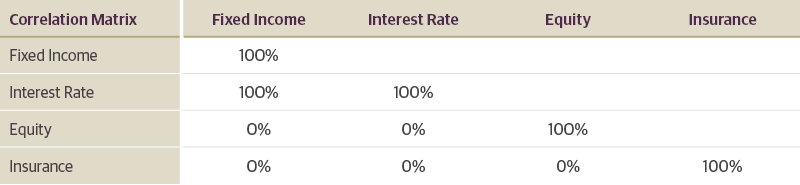

In constructing the model, regulators recognized that not all risks are additive and allowed for diversification benefits. Yet a simplifying assumption was made without nuance. Risks are considered either 100 percent correlated or entirely independent. It is this set of assumptions that regulators are reconsidering. The NAIC is looking to review all the assumptions underlying the formula, which are set forth in the following correlation matrix. In its most recent presentation in October, the AAA compared many capital frameworks’ treatment of correlation assumptions. For simplicity, in our analysis we compared the NAIC’s assumptions to the treatment under the Solvency II model, Europe’s equivalent of RBC, which allows for only a 50 percent correlation between investment categories like stocks and fixed income and a 50 percent correlation between interest rate and credit risk. Altering the RBC model to mirror the Solvency II assumptions would have significant implications.

Investment Risk Correlation Assumptions Under Current RBC Model

Investment Risk Correlation Assumptions Under Current RBC Model

To isolate the significance of the potential change, we compare two components that are currently viewed independently, and how various correlation assumptions would affect a company’s required capital and the resulting RBC ratio.

The calculation for required capital, the denominator of the RBC ratio, is:

Affiliate Risk + Business Risk + [(Other Investment Risk + Interest Rate Risk)2 + (Common Stock + C-3c) 2 + (C-2)2 + (C-3b)2 + (C-4b)2]^(1/2).

Fixed-income risks and interest rate risks are 100 percent correlated and therefore additive. For annuity dominant companies, risks are concentrated in those two buckets and therefore diversification benefits are limited. Under the current model, annuity writers may see only 15 percent reductions in required capital based on the correlation assumptions. Life insurance writers, on the other hand, have a more balanced group of risks with significant exposure to insurance risks, or C-2 , thereby providing a further reduction in required capital.

Assessing the Diversification Benefit

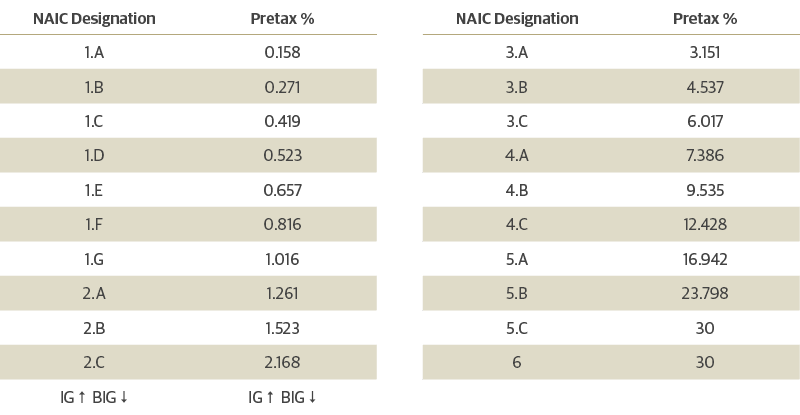

The capital factor for common stock is 30 percent. This is many multiples of the requirement for an investment-grade corporate bond. At a cursory level, this capital factor limits an insurer’s ability to invest in common stocks. Yet the nominal 30 percent is reduced significantly on an after tax and diversification basis. With a very low level of equity allocation, an insurer can add equities to the balance sheet and attract a minimal 3.A–3.C level risk factor or better.

RBC Risk Factor Levels

Source: NAIC. IG = investment grade and BIG = below investment grade.

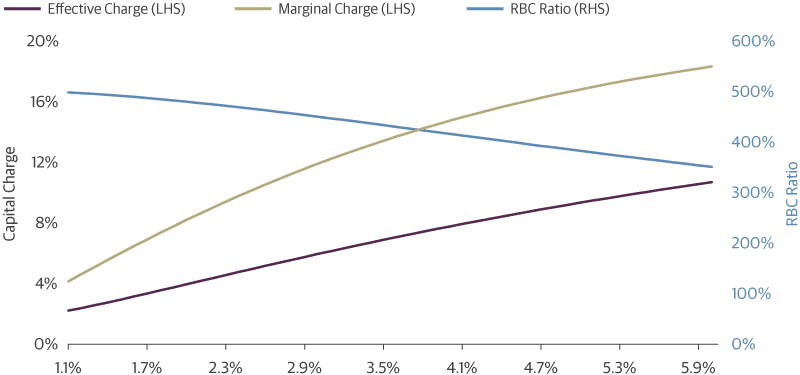

The benefits of diversification, however, wane as exposure increases. We partner with our clients to assess the appropriate level of equity allocation considering the use of capital and the target RBC ratio. The chart below illustrates how the marginal equity capital charge could change for an annuity dominant insurer that reallocated increasing levels of 1.G-2.B designated fixed income toward equities. The marginal capital charge at high levels of exposure runs asymptotic to the after-tax capital charge, but at low levels of exposure the charge is in the single digits. Even at 3 percent of invested assets, the net effective capital charge would be only 6 percent for the aggregate exposure. As the required capital increases with the increasing equity allocation, the RBC ratio declines.

RBC Ratio Declines as Allocation to Equities Rises

Source: Guggenheim Investments, NAIC.

The Impact of Changes to the RBC Model Will Be Meaningful

Changing the investment risk correlation assumptions could significantly increase required capital and reduce life insurer RBC ratios. We believe some insurers, particularly those tight on capital, would need to reassess common stock allocations.

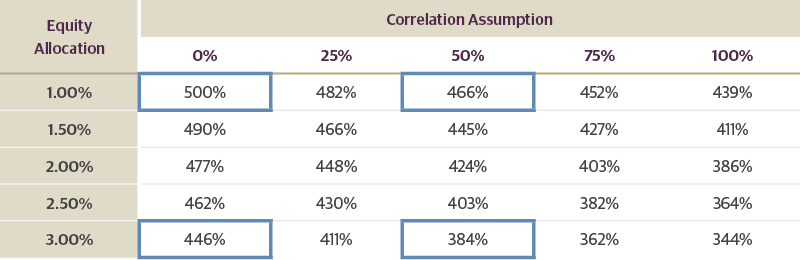

Consider the matrix below that shows how differences in correlation assumptions between equities and fixed income and varying equity allocations impact the RBC ratio for a hypothetical insurer. The hypothetical insurer begins with 1 percent of invested assets in equity and a 500 percent RBC ratio. For this company the difference between the current NAIC assumption that the risks are independent and the Solvency II standard of a 50 percent correlation would be a 34 percentage point reduction in RBC. As the equity allocation increases the difference also increases. At a 3 percent allocation, a shift in the correlation assumption toward the Solvency II model would lead to a 62 percentage point reduction in RBC.

RBC Ratio Declines in 50% Correlation Scenario

Source: Guggenheim Investments, NAIC.

The impact is less severe, although still significant, for a company that attempts to maintain a more modest 350 percent RBC. Under the same set of assumptions—50 percent correlation/1 percent of invested assets in equity—the RBC ratio would decrease by 24 percentage points.

RBC Ratio Declines Are Less at Lower RBC Levels

Source: Guggenheim Investments, NAIC.

Other Changes Are Also Likely

The investment risk correlation assumption is not the only one being reviewed. The NAIC is looking to review all the assumptions underlying the formula. While some changes will lead to a decrease in the RBC ratio as described above, others will cause it to increase. For example, under the NAIC model, fixed-income and interest rate risk are 100 percent correlated thereby providing no diversification benefit. The AAA noted that this compares to a 50 percent correlation under Solvency II. If the NAIC working group decides to move assumptions more in line with the Solvency II model, annuity writers would see diversification benefits emanating from its two largest exposures and the RBC ratios would increase.

Investment Implications

Only time will tell what the ultimate correlation factors will be and how they will impact strategic asset allocations. But if the changes are expansive and mirror assumptions under the Solvency II model, there are likely to be significant changes to companies’ RBC ratios. To avoid unintended consequences, the NAIC should undertake a carefully planned approach with industry input and significant testing. The AAA in October published a comparison to the correlation assumptions in other capital frameworks, which will likely influence regulatory action in the United States. At Guggenheim Investments we are committed to following and reporting on these developments, working with clients to understand the potential repercussions, and evaluating and shifting strategic asset allocations if necessary.

About Insurance Portfolio Management Insights

Insurance Portfolio Management Insights (IPM) provides timely information on topics affecting insurance portfolio management, including regulatory updates, accounting practices and procedures, risk-based capital investment risk and evaluation, financial stability concerns, valuation of securities, reporting, valuation, and market dynamics.

Important Notices and Disclosures

A Record Supply Year Is Taking Shape on Solid Ground

How record credit issuance may reshape market dynamic in 2026.

AI’s Promise and History’s Lessons

The AI investment surge echoes past tech revolutions, but monetization timeline remains uncertain.

First Quarter 2026 Fixed-Income Sector Views

Relative value across the fixed-income market.

Tune in to Macro Markets to hear the top minds of Guggenheim Investments offer timely analysis on financial market trends. Guests include portfolio managers, fixed income sector heads, members of the Macroeconomic and Investment Research Group, and more.

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to interest rate risk. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. Longer term bonds are more sensitive to interest rate changes and subject to greater volatility than those with shorter maturities. During periods of declining rates, because the interest rates on floating rate securities generally reset downward, their market value is unlikely to rise to the same extent as the value of comparable fixed rate securities. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

One basis point is equal to 0.01 percent.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy or, nor liability for, decisions based on such information.

Not FDIC Insured | Not Bank Guaranteed | May Lose Value

© 2024, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim Partners, LLC. For information, call 800.345.7999 or 800.820.0888.

62951

The Advantages of Investing in Infrastructure and Other Real Assets

Portfolio Management Outlook: Staying Focused Amid Geopolitical Uncertainty