/institutional/perspectives/macroeconomic-research/macroeconomic-research-fundamentals-are-solid

Macroeconomic Update: Fundamentals Are Solid, but Policy Uncertainty Is Elevated

We see moderate growth in the U.S. economy in 2025.

The U.S. economy has good momentum heading into 2025, but the policy outlook from Washington elevates uncertainty. Recent economic data have been solid, with fourth quarter real gross domestic product (GDP) on track for about 2 percent annualized growth. The outlook for consumer spending remains positive, supported by healthy growth in inflation-adjusted labor income and a wealth effect driven by rising asset prices. Financial conditions have also turned more supportive as credit growth is reaccelerating, and optimism about artificial intelligence induces a positive outlook for capex. Disinflationary progress has stalled a bit in recent months, but fundamentals point to a further slowdown in inflation as wage pressures and housing inflation ease further.

With the new administration taking office, we expect a boost to both consumer and business sentiment, aided by expectations of deregulation and further tax cuts. Post-election surveys have already shown increased optimism about the outlook, which could support consumption, investment, and hiring in coming months.

Looking beyond the immediate sentiment boost, the outlook becomes more uncertain and depends on the ultimate policy mix of the new administration. Extension of the Tax Cuts and Jobs Act (TCJA) would prevent a fiscal drag, but we see limited scope for new tax cuts as the fiscal backdrop has worsened.

Some of the administration’s proposed policies—such as tariffs and immigration—could weigh on growth if fully implemented. Tariffs slow growth by increasing business uncertainty and lowering real incomes. Broad implementation of tariffs could also threaten to push up prices, complicating the Fed’s task of returning inflation to 2 percent and potentially slowing the pace of rate cuts. Ultimately, we expect more targeted tariffs will be used to negotiate favorable terms for the United States. Immigration activity at the border is already down over 70 percent from its 2023 peak, which should slow both labor supply and consumption in coming quarters. Our expectation is that additional new policies will slow immigration modestly further than the current trajectory.

All together, we see moderate growth in the U.S. economy in 2025 as these policy shifts play out. Economic fundamentals remain solid, with strong household and corporate balance sheets. The Fed will likely ease policy further toward a neutral setting, but tariffs could slow the pace of rate cuts by interrupting the disinflationary trend. The U.S. economy should remain a global outperformer, though we expect continued bifurcation across sectors, particularly as new policies begin to have an impact.

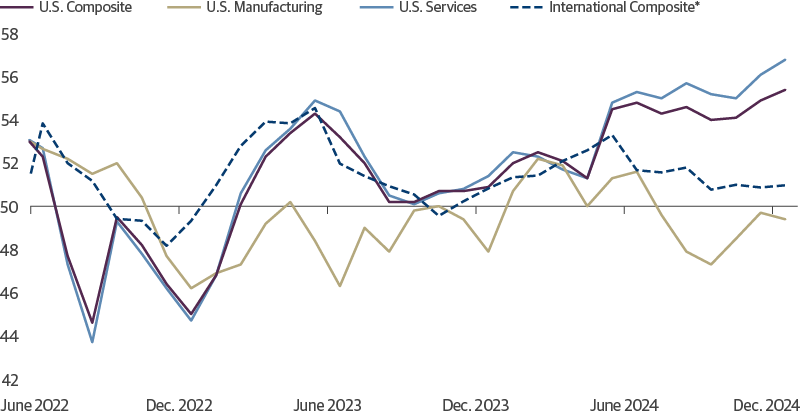

U.S. Growth a Bright Spot, Led by Strong Services Sector

With the new administration taking office, we expect a boost to both consumer and business sentiment, aided by expectations of deregulation and further tax cuts.

Source: Guggenheim Investments, S&P Global, Bloomberg. Data as of 12.31.2024. *International is a simple average of China, Eurozone, Japan, and Emerging Markets. PMI = Purchasing Managers Index.

—By Matt Bush and Maria Giraldo

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the authors, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Investing involves risk, including the possible loss of principal. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. Longer term bonds are more sensitive to interest rate changes and subject to greater volatility than those with shorter maturities. During periods of declining rates, the interest rates on floating rate securities generally reset downward and their value is unlikely to rise to the same extent as comparable fixed rate securities. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, and GS GAMMA Advisors, LLC.

GPIM 63636

Tune in to Macro Markets to hear the top minds of Guggenheim Investments offer timely analysis on financial market trends. Guests include portfolio managers, fixed income sector heads, members of the Macroeconomic and Investment Research Group, and more.

©

Guggenheim Investments. All rights reserved.

*Assets under management is as of 12.31.2024 and includes leverage of $14.8bn. Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Wealth Solutions, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Private Investments, LLC.

By choosing an option below, the next time you return to the site, your home page will automatically

be set to this site. You can change your preference at any time.

We have saved your site preference as

Institutional Investors. To change this, update your

preferences.

United States Important Legal Information

By confirming below that you are an Institutional Investor, you will gain access to information on this website (the “Website”) that is intended exclusively for Institutional Investors and, as such, the information should not be relied upon by individual investors. This Website and any product, content, information, tools or services provided or available through the Website (collectively, the “Services”) are provided to Institutional Investors for informational purposes only and do not constitute a recommendation to buy or sell any security or fund interest. Nothing on the Website shall be considered a solicitation for the offering of any investment product or service to any person in any jurisdiction where such solicitation or offering may not lawfully be made. By accessing this Website, you expressly acknowledge and agree that the Website and the Services provided on or through the Website are provided on an as is/as available basis, and except as partnered by law, neither Guggenheim Investments and it parents, subsidiaries and affiliates nor any third party has any responsibility to maintain the website or the Services offered on or through the Website or to supply corrections or updates for the same. You understand that the information provided on this Website is not intended to provide, and should not be relied upon for, tax, legal, accounting or investment advice. You also agree that the terms provided herein with respect to the access and use of the Website are supplemental to and shall not void or modify the Terms of Use in effect for the Website. The information on this Website is solely intended for use by Institutional Investors as defined below: banks, savings and loan associations, insurance companies, and registered investment companies; registered investment advisers; individual investors and other entities with total assets of at least $50 million; governmental entities; employee benefit (retirement) plans, or multiple employee benefit plans offered to employees of the same employer, that in the aggregate have at least 100 participants, but does not include any participant of such plans; member firms or registered person of such a member; or person(s) acting solely on behalf of any such Institutional Investor.

By clicking the "I confirm" information link the user agrees that: “I have read the terms detailed and confirm that I am an Institutional Investor and that I wish to proceed.”